Credit Cards I’m Keeping

The credit card world has changed a lot since I started accumulating sign up bonuses about six years ago. Banks have cut down on the ability to churn (open a card, get the bonus, close it, then reopen it for another sign up bonus). The pandemic has made travel benefits less lucrative.

Today I closed another card, my Chase IHG+ card I have had for three years. I just couldn’t justify paying another year of the $89 annual fee when I am not staying at IHG properties and the price of award stays has gone up.

I tend to keep cards that don’t have an annual fee. I figure I might use them if there is a good offer (Amex & Chase Offers) on the card.

Of the various bank currency, I find Chase Ultimate Rewards to be the most lucrative for me as I can transfer them to World of Hyatt points which I burn through. I have a small bank of Amex Membership Rewards but rarely find a use for them. I no longer collect Citi ThankYou points though I did like when you could use them to book flights for 1.25 cents each. I don’t have experience with other bank currency.

For cash back, I tend to like the Citi Costco and Discover It cards the best. For co-branded cards, I like Hyatt and Alaska Airlines points. I really only use my IHG or Hilton cards for spend at those specific properties which is a rare occasion.

Credit Cards I Currently Hold

*Cards that hold a permanent spot in my wallet

- *Chase Hyatt ($95 annual fee) – Hyatt is my hotel brand of choice. The annual Category 1-4 certificate typically makes the annual fee worth it to me along with the bonus points on Hyatt properties and in restaurants. This tends to be the card I keep in my wallet for every day spend.

- Chase IHG Select ($49 annual fee) – While I closed the higher fee version, the grandfathered $49 version gets me an annual free night certificate (up to 40,000 points). I’ve been finding that IHG has raised their rates and now it is difficult to find a nice property under the 40k points (in fact I am likely going to have some free nights expire this year unless I do a staycation), but even if it is a Holiday Inn stay once a year, I can make the annual fee worthwhile in most years. This card only ends up in my wallet if I have an IHG stay coming up.

- Chase Sapphire Preferred ($95 annual fee) – This is my newest card that I signed up for when there was an 80,000 Ultimate Rewards sign up bonus (now it is 100,000 points, so I should have waited). I may cancel it once the year is up, though with the new 10% annual bonus points, I may keep it one more year. This card is my other every day spend card that stays in my wallet.

- Chase Freedom (No annual fee) – This was formerly my Chase Sapphire Reserve which I downgraded before the first year to avoid the annual fee in 2017. Rarely put spend on it.

- Chase Freedom Unlimited (No annual fee) – Rarely put spend on it but no annual fee.

- Chase Ink Business Cash (No annual fee) – Rarely put spend on it but every once in a while I use it as at an office supply store. If there was an annual fee I would close it.

- Amex EveryDay (No annual fee) – Rarely put spend on it, but use it when there is a good Amex Offer and there is no annual fee.

- Amex Blue Business Plus (No annual fee) – Same as other no fee Amex cards.

- Amex Hilton Honors (No annual fee) – Same as other no fee Amex cards.

- *Citi Costco (No annual fee) – Use it for purchases at Costco and gas (4% annual cash back). This is one that has a permanent home in my wallet since I go to Costco and gas up a few times a month.

- *Discover It (No annual fee) – Use it for quarterly bonuses. Typically stays in my wallet if the quarterly bonus is restaurants.

- Bank of America Alaska Airlines ($75 annual fee) – Keep it for the annual companion fare and for Alaska Airlines purchases.

- Bank of America Amtrak ($79 annual fee) – just opened this card for the 50,000 Amtrak points plus $100 statement credit. I am hoping to take more Amtrak trips and this is a great way to do it. But will close it before the anniversary date.

One thing you may notice is that none of my cards have an annual fee over $100. That means I don’t have any premium cards that give me access to airport lounges through Priority Pass or the Centurion Lounge. I might consider reapplying for the Chase Sapphire Reserve once/it the sign up bonus hits 100k again but I just don’t see the long term value in any of the premium cards on the market right now.

Credit Cards I’ve Had But Closed or Downgraded due to Annual Fees

- Chase IHG+

- Chase Iberia

- Chase Sapphire Reserve (downgraded)

- Chase Fairmont

- Amex Hilton Honors Plus

- Amex Platinum

- Amex SPG

- Amex Delta

- Barclay Arrival+

- Barclay JetBlue

- Citi Prestige

- Citi Premier

- Citi Hilton

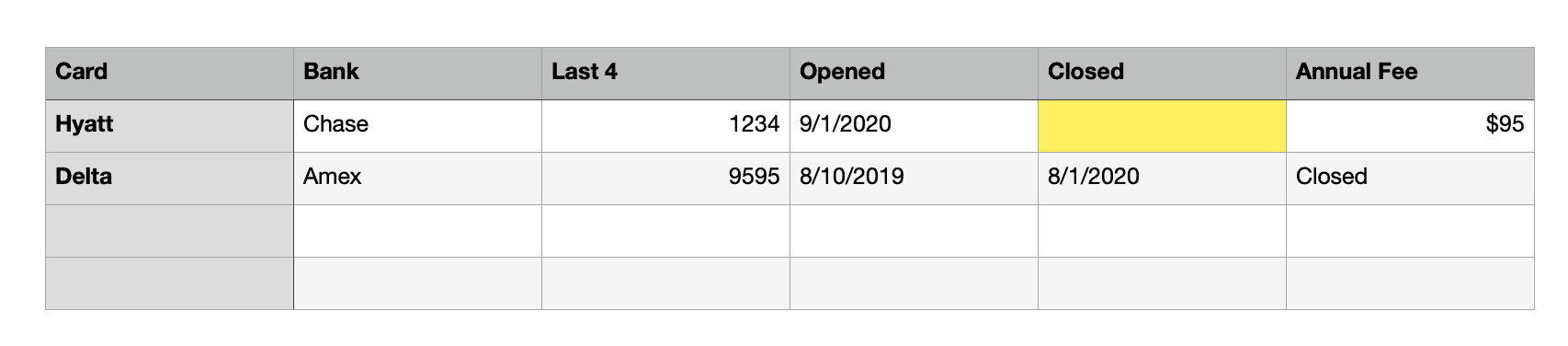

With all of the cards I currently hold and ones I have closed, I find it is important to keep a spreadsheet of my cards. I use a simple spreadsheet with six columns that looks something like this:

It allows me to quickly check the anniversary dates of cards (when the annual fee is due) so that I can make sure to close it (or at least evaluate if it is worth keeping for another year). If the card is open, I shade the cell for closed date as yellow to make it easier to find.

If you can’t remember when you opened a card or the history of cards you have held and closed, you can get a good amount of info off your free credit reports from one of the big three credit bureaus.

What is your plan for opening and closing cards? Do you have a system for tracking your credit cards?

Notice: I am not a financial expert and do not offer any financial advice. I do not receive any compensation for any of my posts.